Section 529 Plan Distribution Rules

How To Withdraw From Your 529 Plan

529 Plan Distribution Flowchart Flow Chart How To Plan 529 Plan

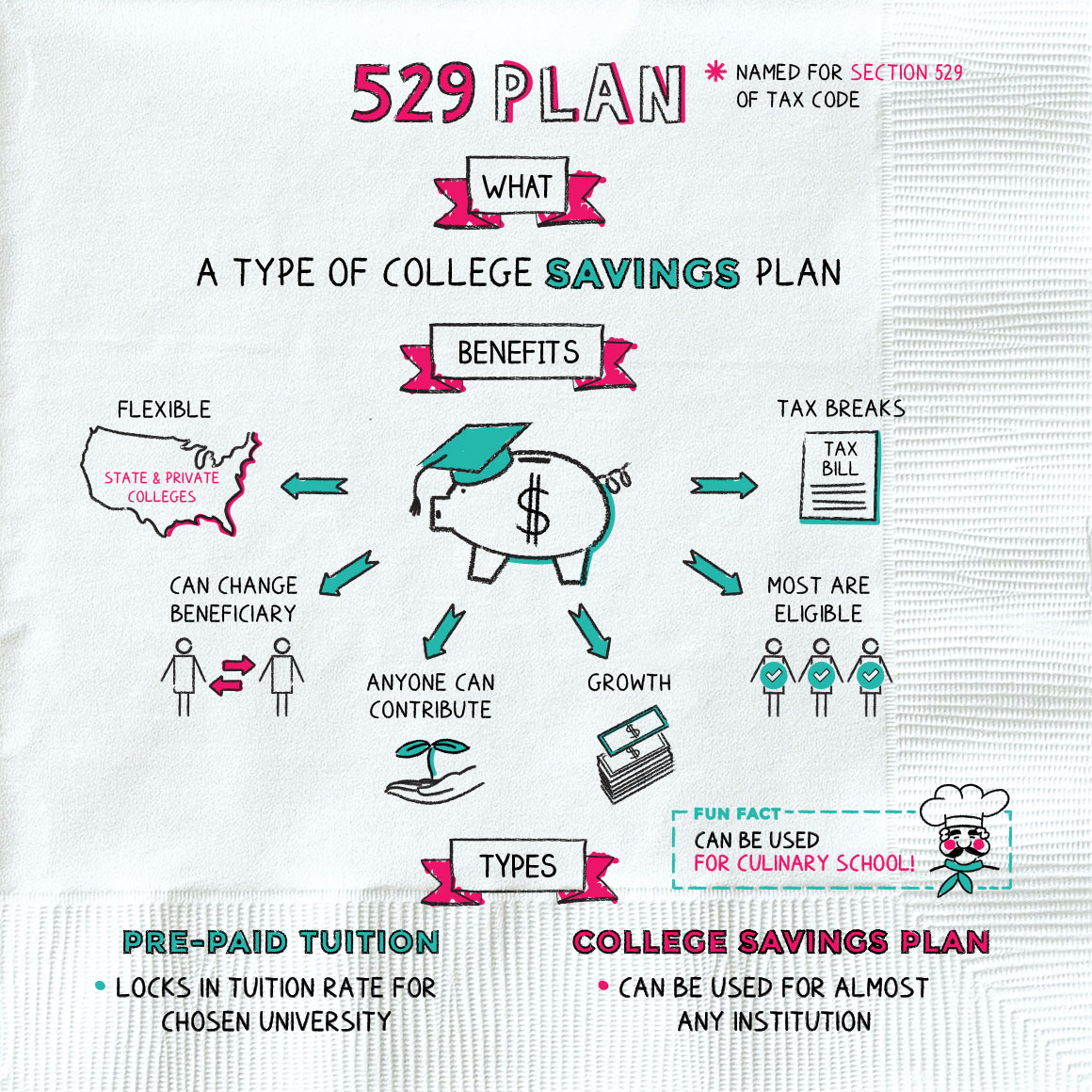

529 Plan Napkin Finance

Can I Use A 529 Plan For K 12 Expenses Edchoice

How To Switch 529 Plans

Pin On A Student Savings

Parents can withdraw money from a 529 plan at any time for any reason.

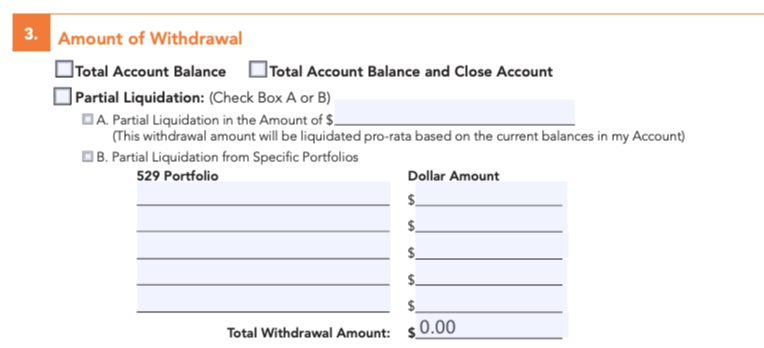

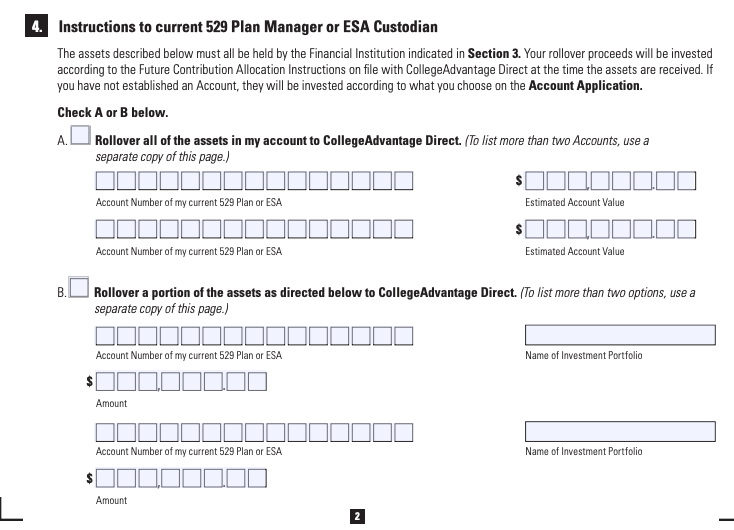

Section 529 plan distribution rules.

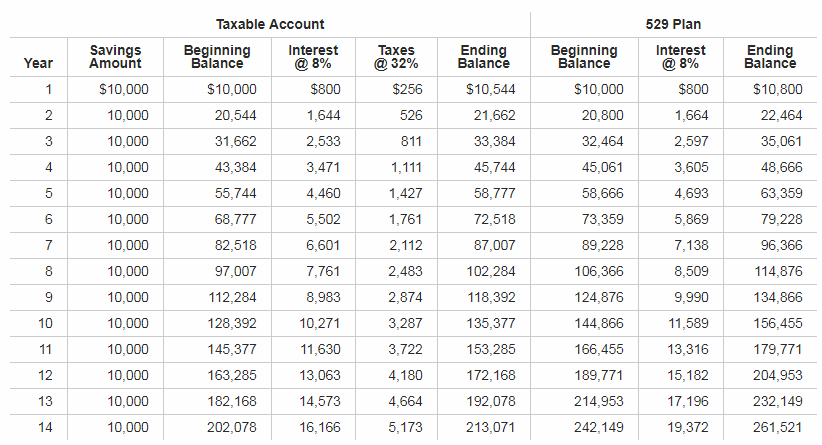

Journal The Financial Impact Of Not Using 529 Plans And Behavioral Interventions To Increase Usage In 2020 How To Plan 529 College Savings Plan Savings Plan

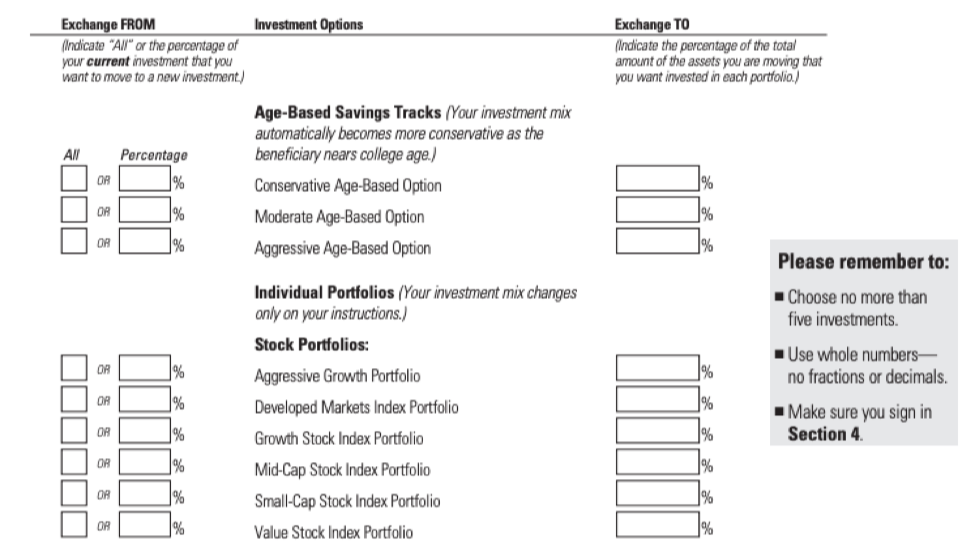

How Many 529 Plan Investment Changes Can You Make Per Year

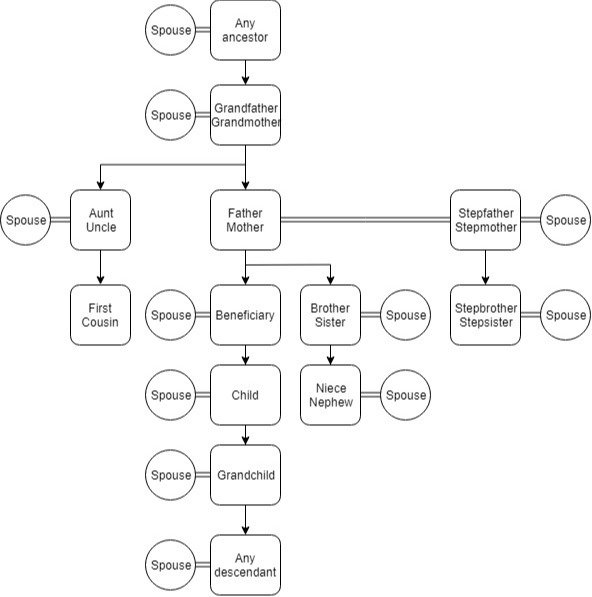

Who Is A Member Of The Family Of A 529 Plan Beneficiary

Path2college 529 Plan Georgia 529 College Savings Plan Ratings Tax Benefits Fees And Performance

529 Plan For Your Grandchildren Baron Law Llc

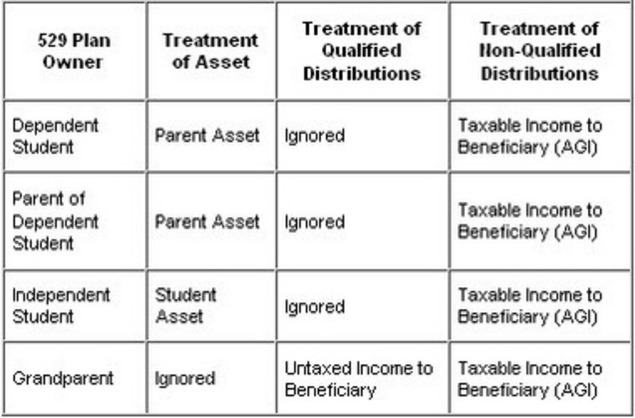

How Do Grandparent Owned 529 College Savings Plans Affect Financial Aid Eligibility Fastweb

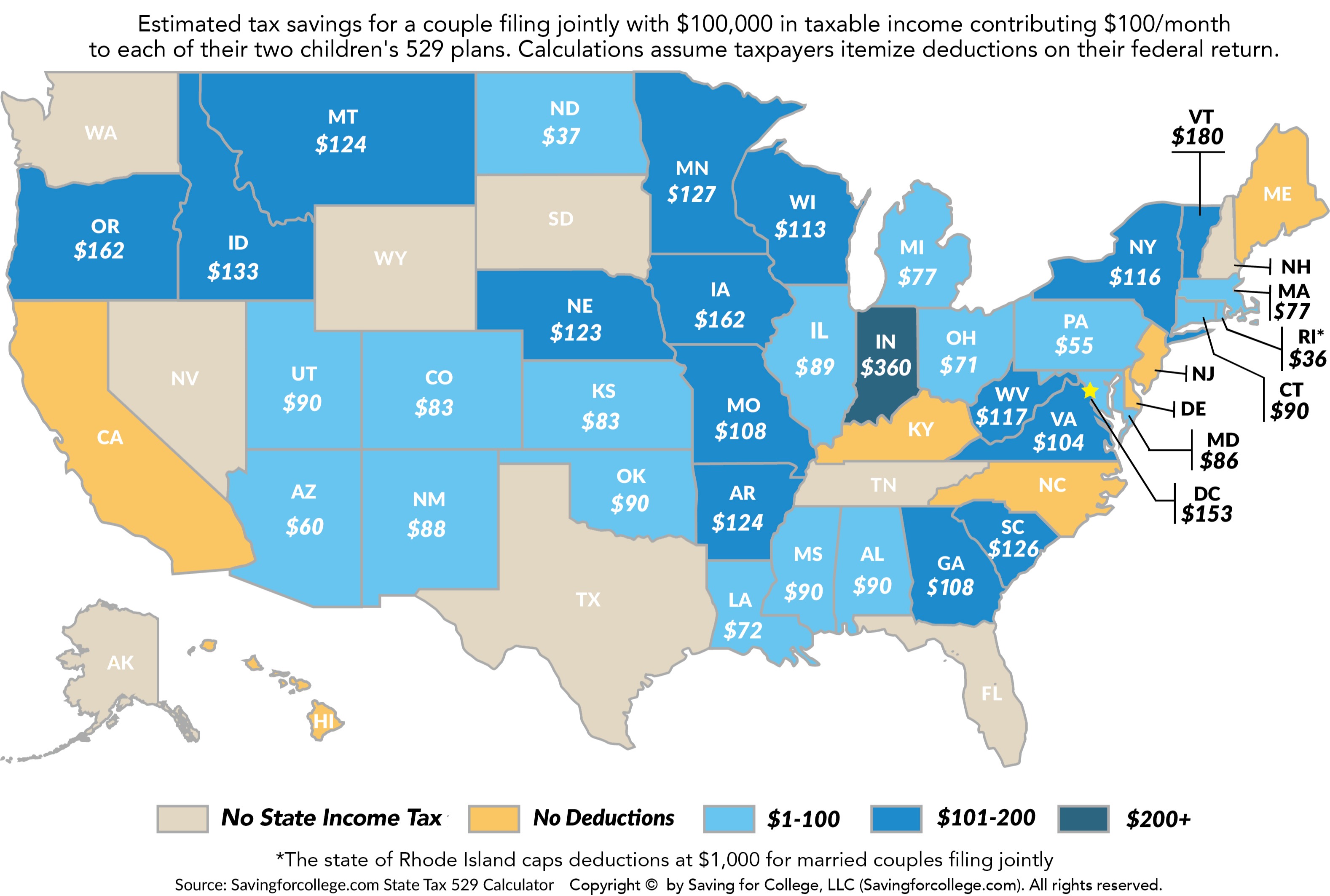

How Much Is Your State S 529 Plan Tax Deduction Really Worth

Collegechoice 529 Direct Savings Plan Indiana 529 College Savings Plan Ratings Tax Benefits Fees And Performance

Gift College Investing Plan Arkansas 529 College Savings Plan Ratings Tax Benefits Fees And Performance

What S A 529 College Savings Plan 529 College Savings Plan Education Savings Account Saving For College

About 529 College Savings Florida 529 Plan Florida Prepaid

What Are Qualified Expenses For A 529 Plan And What Doesn T Count

529 Plan Vs Life Insurance How To Plan 529 Plan Financial Aid For College

The Secure Act And 529 Plans Articles Advisor Perspectives

Nevada Nv 529 Plans Fees Investment Options Features Smartasset Com

Scholars Choice 529 College Savings Faqs Legg Mason

Education Financial Planning Required Insight For The 529 Industry 529conference In 2020 Financial Planning 529 College Savings Plan Saving For College

Https Www Schwab Com Public File P 746543

Pin By Melisa Adrien On College In 2020 How To Plan Word Search Puzzle Education

Grandparents Faqs On 529s College Savings For Grandchildren

Iadvisor 529 Plan Iowa 529 College Savings Plan Ratings Tax Benefits Fees And Performance

College Save Direct North Dakota 529 College Savings Plan Ratings Tax Benefits Fees And Performance

Ohio S 529 Plan Collegeadvantage Ohio 529 College Savings Plan Ratings Tax Benefits Fees And Performance

Frequently Asked Questions Arizona College Savings Plan

Can You Use A 529 To Pay For College Overseas

529 Dash E Newsletter On 529 Plans And Able Accounts For Week Of April 2 2018 529 College Savings Plan Saving For College College Savings Plans

Ny 529 Direct Plan Offers College Savers Tax Benefits Low Contribution Minimums Flexibility And Low Costs Saving For College How To Plan College Costs

Understanding Your 401 K Statement Inside Your Ira Here S A Guide To Understanding Your 401 K Statement Investing Investing For Retirement Ira Investment

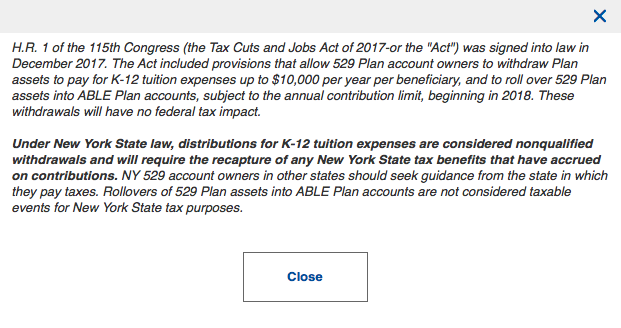

Ny Taxpayers Be Careful About Using 529 Money For K 12

Vermont Higher Education Investment Plan Vermont 529 College Savings Plan Ratings Tax Benefits Fees And Performance

The 2019 Calendar Has Been Released By Nest 529 College Savings Plan First National Bank Of 529 College Savings Plan Saving For College College Savings Plans

529 Plan Putnam Investments

Maryland 529 Maryland Senator Edward J Kasemeyer College Investment Plan Maryland 529 College Savings Plan Ratings Tax Benefits Fees And Performance

Washington Dc Dc 529 Plans Fees Investment Options Features Smartasset Com

College Savings Iowa Iowa 529 College Savings Plan Ratings Tax Benefits Fees And Performance

How To Use A 529 Plan If A Child Does Not Go To College Investing To Thrive

Rcb Bank S Mary Wood Explains Some Of The Best Uses For Your Tax Refund A 529 Education Savings Plan Is Ideal If You Re Plann In 2020 Tax Refund Education Savings Plan

Basics Of 529 Plans And Options For Washington State Bader Martin

Understanding Full Ride And Full Tuition Scholarships Road2college Financial Aid For College Scholarships For College Scholarships

It S College Savings Day Are You Saving Enough For Your Children S Education Saving For College Financial Aid For College Education Savings Account

Secure Act Retirement Planning Opportunities And Challenges Retirement Planning Lifetime Income Financial Advisors

Should You Use A 529 Plan For Elementary And High School

Click To Learn More About The Event 529 College Savings Plan Saving For College College Savings Plans

401 K Early Retirement Guide Inside Your Ira We Ve Got The Lowdown On Your 401 K Early Retirement Qu Investing For Retirement Early Retirement Retirement

Source : pinterest.com