Section 42 Tax Credit Lihtc Housing Program

Low Income Housing Tax Credit Ihda

Lihtc Low Income Housing Tax Credit Program Compliance Ppt Download

Http Nlihc Org Sites Default Files Ag 2018 Ch05 S09 Lihtc 2018 Pdf

Irc Section 42 Low Income Housing Tax Credits And Irc Section 47 Hist

Low Income Housing Tax Credit Program Overview Pdf Free Download

Low Income Housing Tax Credit Program Virginia Housing

Projects serving low income.

Section 42 tax credit lihtc housing program.

Home And The Low Income Housing Tax Credit Guidebook Pdf Free Download

Low Income Housing Tax Credit Ppt Download

Low Income Housing Tax Credits Nhlp

Low Income Housing Tax Credit Program Wvhdf

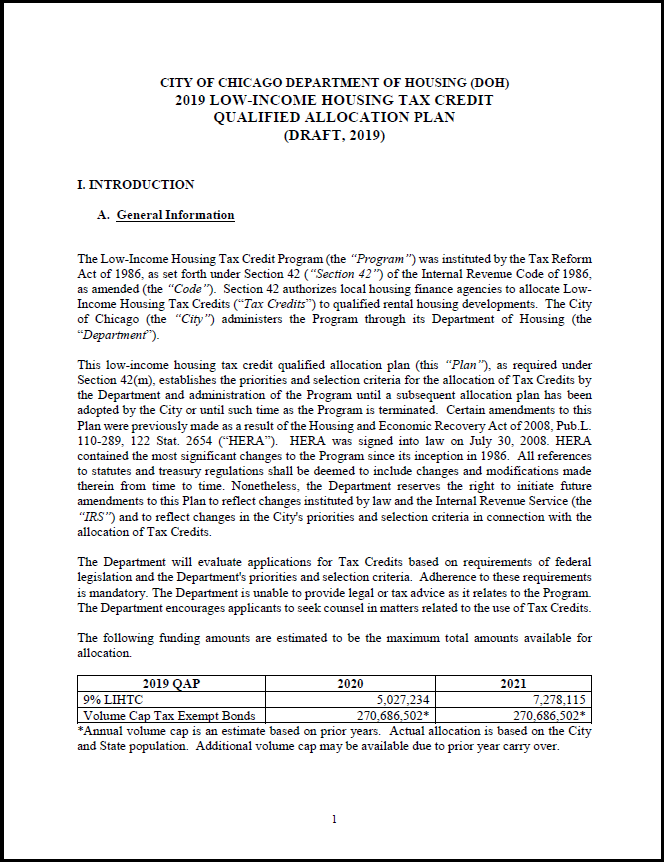

City Of Chicago Qualified Allocation Plan

Low Income Housing Tax Credit Toolkit Open Communities Alliance

An Introduction To The Housing Tax Credit Program Part 1 Ppt Download

Https Dhcd Dc Gov Sites Default Files Dc Sites Dc Page Content Attachments Lihtc 20owners 20cert 20of 20continuing 20program 20compliance 202017 Pdf

Https Www Ahcinc Net Schra 202020 20compliance 20manual Pdf

Section 8 Vs Section 42 National Center For Housing Management

Beginner S Guide To Lihtc Ppt Download

Https Www Lhc La Gov Hubfs Document 20libraries Housing 20development Funding 20opportunities Qap Draft 20policy 20brief 4 20percent 20and 20mrb 20 20april 2016 202019 Pdf

Https Www Nhlp Org Wp Content Uploads Ohio Lihtc Lawsuit Pdf

Low Income Housing Tax Credit Ndhousing

When To Consolidate A Not For Profit S Interest In Low Income Housing Projects Marks Paneth

Gliha Training August Ppt Download

An Introduction To The Low Income Housing Tax Credit Everycrsreport Com

Louisiana Housing Corporation Overview Of Lhc Resources June 9 Ppt Download

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcspj2fn2aqvhnoptjm D4omib4u1bawpp7r0bqfkfrqtrp0m N2 Usqp Cau

Life Of An Lihtc Project In 60 Minutes Ppt Download

Irs Provides Section 42 Covid 19 Relief National Center For Housing Management

Http Www Iaao Org Library Library Files Lihtc Subject Guide Updated2018 Pdf

Https Www Wheda Com Globalassets Documents Tax Credits Htc Introduction To Lihtc Pdf

Https Www Energy Gov Sites Prod Files 2019 10 F67 3 Lihtc Nmtcforcleanenergy Pdf

Novogradac Low Income Housing Tax Credit Handbook 2016 Edition Paperback 2016 Michael J Novogradac Cpa 9780314647191 Amazon Com Books

End Of Year Tax Planning For Lihtc Properties Novogradac

Irs Form 8823 And The 8823 Guide National Center For Housing Management

Local Court Win Is A Victory For Affordable Housing Communities Nationwide

Valuation Of Low Income Housing Tax Credit Developments Lihtc 101 Tickets Wed Nov 4 2020 At 10 00 Am Eventbrite

Nvhousingsearch Org 2019 Annual Report On Nevada Lihtc Housing

:max_bytes(150000):strip_icc():saturation(0.2):brightness(10):contrast(5)/Buildinglowincomehousing-6db4ba4400c340c7bc277c872b68e1a8.jpg)

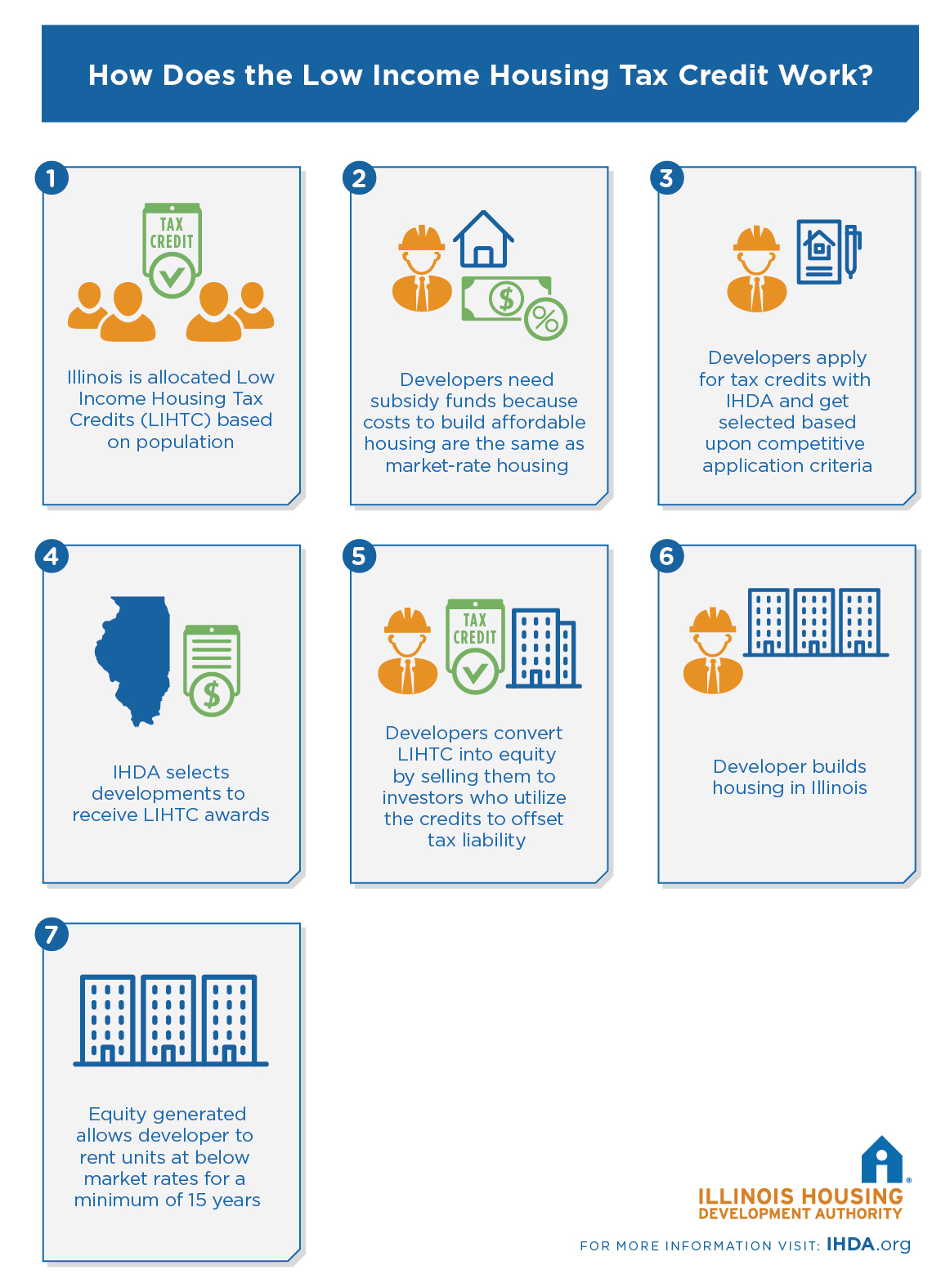

How Does The Low Income Housing Tax Credit Work

Hud Lihtc And Usda Rd Updates For Covid 19 Outbreak Us Housing Consultants

Tax Credit Percentages 2016

Citybizlist Washington Dc Greysteel Arranges The Sale Of A 100 Unit Senior Affordable Housing Property In Baltimore Md For 7 7m

Http Www Mainehousing Org Docs Default Source Msha Rules Ch 16 Low Income Housing Tax Credit Rule Pdf

Low Income Housing Tax Credits Lihtc Explained In 2 Minutes Youtube

Sell Lihtc Property Archives Affordable Housing Investment Brokerage

Zonnie S Resume

Https Www Nahma Org Wp Content Uploads Files Member Nn 20articles Tc 20jul 20aug08 Nahmanews Lores Pdf

Https Www Novoco Com Sites Default Files Atoms Files New Jersey 2017 Final Qap 030617 Pdf

Https Www Novoco Com Sites Default Files Atoms Files Carolina Planning Article Critiquing The Critique 030108 Pdf

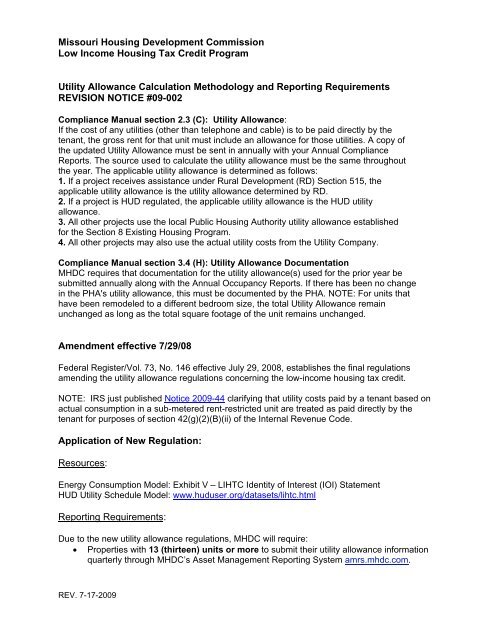

Revision Notice 09 002 A Utility Allowance Calculation Missouri

Interpreting The Average Income Test Part 1 Novogradac

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcrtdwyadoytfctfuro7ycdeg9sliwkqaqqge81 Vum16j9qttil Usqp Cau

Source : pinterest.com