Section 1031 Of The United States Internal Revenue Code

What Is A 1031 Exchange Asset Preservation Inc

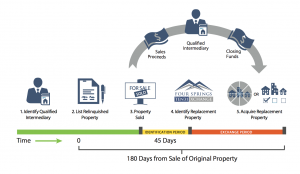

How To Do A 1031 Exchange Rules Definitions For Investors 2020

Why Use The Irc 1031 Exchange Real Estate Transition Solutions

A Primer In Internal Revenue Code 1031 And The Art Of The Deal For Real Estate Investors Propertyshark Real Estate Blog

The Ultimate Guide To 1031 Exchanges Real Estate Investing Real Estate Investment Group Investing

United States Internal Revenue Code 26 U S C 1031 Deferral Opportunities Teeple Hall

D basis if property was acquired on an exchange described in this section section 1035 a section 1036 a or section 1037 a then the basis shall be the same as that of the property exchanged decreased in the amount of any money received by the taxpayer and increased in the amount of gain or decreased in the amount of loss to the taxpayer that was recognized on such exchange.

Section 1031 of the united states internal revenue code.

Ml80yx5 I7mqgm

What Is A 1031 Exchange Mark D Mchale Associates

Silverhawk Private Wealth What Is A 1031 Exchange Silverhawk Private Wealth

1031 Exchange Details Cai Investments

Internal Revenue Code Section 1031 Wikiwand

Section 1031 Update Proposed Regulations And The Covid 19 Relief Extension Date

Section 1031 Exchange Transactions Regulations And Advantages

How Seasoned Investors Leverage The 1031 Exchange As A Tax Shelter Life Learning Leverage

1031 Exchange Rules Tax Deferred Exchange Manhattan Miami

Filing Taxes Late Penalty Calculator Http Www Irstaxapp Com Filing Taxes Late Penalty Calculator Filing Taxes Internal Revenue Code Tax

1031 Exchange Bestreich Realty Group

History Of The 1031 Exchange

Pin By Abhishek Jain On Tax Guru Budgeting Business Google Play

Frequently Asked Questions Faqs About 1031 Exchanges

Sponsored How To Successfully Defer Taxes In A 1031 Exchange The Di Wire

6 Strategies To Defer And Or Reduce Your Capital Gains Tax When You Sell Real Estate Lifeafar Investments

Https Www Efirstbank1031 Com Documents 1031exchangemanual Pdf

Agent And Broker Growth Increased Realty Real Estate Agent Real Estate

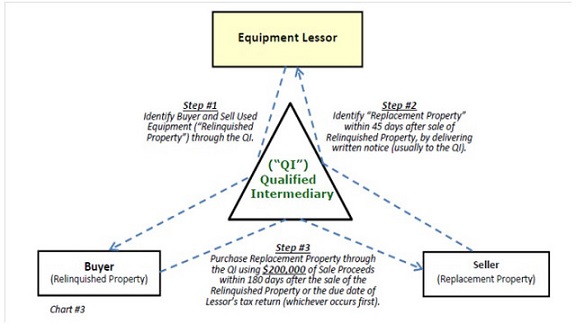

Limit Taxes On Sale Of Rental Equipment

The Real Impact Of House Flipping Infographic Real Estate Investor Real Estate Investing Real Estate Infographic

Addressing Confusion About 1031 Exchanges

Principles Of Good Lending Bank Lending Commercial Bank Lending

Cpa Academy

Properties Of Financial Assets The Properties And The Pricing Of Financial Assets Can Be Liken To The Financial Asset Financial Statement Analysis Financial

1031 Exchange Invest In Boston Real Estate For Your Exchange

Biden S Tax Plan Would Pull The Rug Out From Under The Real Estate Industry Insiders In 2020 Property Investor Estates Real Estate

1031 Tax Reform Updates Ipx1031

Pin On Company

Want To Sell Your Property Use A 1031 Exchange

1031 Exchange Updates Impacts For 2018 Ipx1031

Failed 1031 Exchange May Qualify For Installment Sale Treatment Under Irc Sec 453 Commercial Partners Title

Tax Cuts And Jobs Act Of 2017

1031 Exchange Rule

1031 Exchange Overview How To Lucas Real Estate

What Is Qualified Like Kind Property In A 1031 Exchange Ipx1031

1031 Exchange Reform Has Become A Campaign Topic Again

Do Co Ops Qualify New York Law Journal Legal 1031

Https Cdn2 Hubspot Net Hubfs 26654 Docs Powerof1031 4 Kwc Pdf T 1496420052390

Capital Square 1031 Launches Dst Offering Of New Class A Apartment Community In Williamsburg Va

Purpose Of 1031 Exchanges

Irs Covid 19 Deadline Extensions Do Not Include Section 1031 Exchanges Yet Brown Fox

1031 Exchanges Tardiflaw

How To Do A 1031 Exchange In Nyc Hauseit New York City

4xqgtjv7zxyyvm

Source : pinterest.com